In July 2021 Advantage Business conducted a Business Sentiment Survey. We ‘asked the audience’ what impact the pandemic was having on New Zealand’s SME sector. Little did we know that New Zealand was heading back into a Level 4 lockdown in August. Had the survey been timed differently it would have produced a very different set of results. What we share with you here is the change in sentiment one year on from our first survey. No doubt next year will tell a different story again…

Quick links

Introduction

The COVID pandemic has now impacted us for more than eighteen months and will be with us for the foreseeable future. A year ago, we conducted a nationwide survey to gauge the impacts at that time on the SME sector within New Zealand. We found, six months into the pandemic, both market conditions and customer behaviours had changed and were continuing to do so in an uncertain environment. Many SMEs were struggling with cash flow and had reduced access to working capital and investment opportunities. Government support for the sector had not met the expectations of small business owners.

Although vaccines are now being rolled out around the world, there are still many uncertainties affecting local businesses, including labour shortages, skill shortages, supply chain issues, new government policies, drastic changes in housing and construction, and very different consumer behaviour.

While our country has done well to contain the local spread of the virus thus far, the outlook for our economy remains uncertain, especially given our border restrictions which affect our interconnectedness with global trade, finance and geopolitics.

Advantage Business is a well-established business advisory company working with small and medium-sized businesses around NZ for over two decades. We want to know, as best possible, what are the current impacts of the pandemic on the SME sector in NZ. That is why we ran our second annual survey to collect data from SME business owners throughout NZ about how COVID and other structural influences will likely affect their businesses over the coming twelve months.

We were most interested in the following issues and how they directly impact SME businesses in New Zealand:

- What are the changing market conditions?

- How have customer behaviours changed?

- Do SMEs have enough cash flow and working capital?

- Are there new investment opportunities?

- Are there any unexpected positive outcomes from the crisis?

- Has their use of technology changed?

- Have levels of government support for SMEs been adequate?

- Has support from the banking sector been adequate?

- What areas need the most support in their business?

Sample

The survey was conducted in July 2021. Participants provided feedback for the twelve months from July 2021 to August 2022. There were 92 respondents from the Advantage Business database, with a regional spread throughout New Zealand.

Results

3.1 CHANGING MARKET CONDITIONS & BORDER CLOSURES

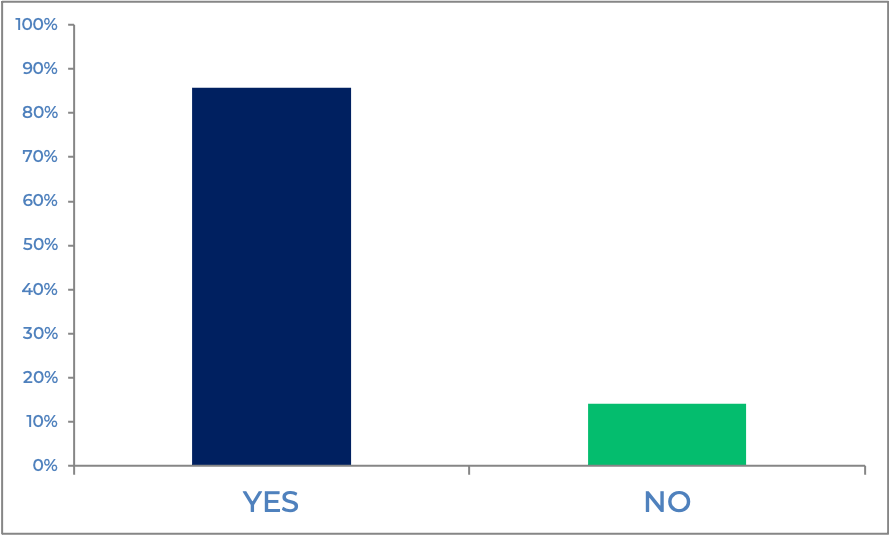

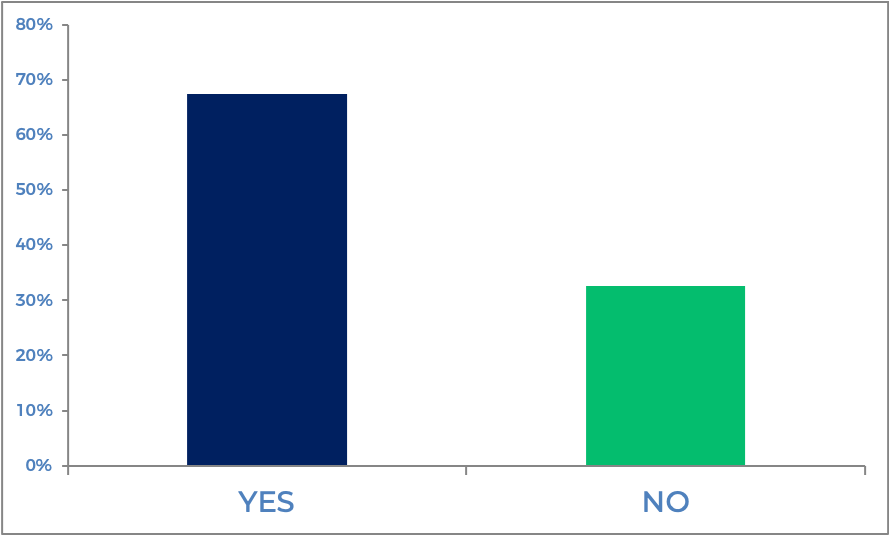

A strong majority (86%) of small business owners believe that changed/changing market conditions will impact their business in the next twelve months. Fourteen per cent believe there will be no change.

Are changed/changing market conditions likely to impact your business within the next 12 months?

When asked for further comments, most respondents thought that changing market conditions would negatively impact their business. While, last year, the most concerns were related to a slowdown of construction and infrastructure projects, this year’s key concerns are both around difficulties in the global and domestic supply chains, and major uncertainties around labour supply. For example:

“Container and air freight cost three times more. We need six times more containers on the water at one time because of arrival delays!”

“Material and labour supply moving forward are an unknown…”

“We are busier but have no staff to ensure timely deliveries…”

“There is a significant lack of staff to hire with no internationals and minimal movement within now within NZ.”

Another concern was around ongoing border closures and the lack of international travel. For example:

“Continued border closures have a negative impact on our business. We are 30% down on last year and likely to be worse this year…”

“We depend on international travellers but we expect them back no sooner than 2023.”

“No international travellers equates to 70% of our income.”

Overall, the theme of most comments is that a significant slowdown in some sectors of the economy is ongoing and the flow-on effects of that slowdown, while still being played out, continues to be very damaging at the small business level.

When asked, “What impact have NZ border closures had for your business?” Fifteen respondents were neutral or positive about the impacts and sixty-four provided negative comments.

Those making positive comments about the impacts of border closures on their business included more money spent by Kiwis on domestic travel and increased demand for local goods and services.

In line with lasts year’s survey, negative comments focused on both direct impacts due to border closures (such as supply and labour issues) and the flow-on effect of other businesses further up the supply chain having an impact as a result. For example:

“Staff issues such as being able to reunite with family and also working visas.”

“We have more work than I could possibly do and not the staff available to do the work I’ve already got…”

“The labour market is much tighter for my clients, so growth is going to be difficult for them…”

“Dramatic reduction in turnover. We have an inability to project if the business will be viable until the borders open.”

3.2 CHANGING CUSTOMER BEHAVIOUR

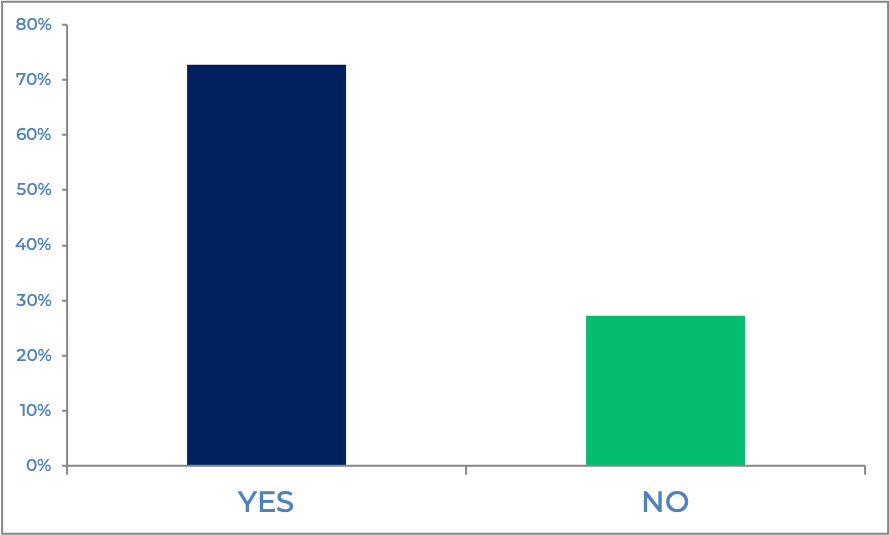

Respondents were asked, “Have there been any recent changes in your customer behaviour that have influenced changes in supply and demand?” A large majority (72.8%) replied ‘yes’, while 27.2% replied ‘no’.

Have there been any ongoing changes in your customers’ behaviour that have influenced changes in supply and demand?

When asked for further comments, respondents reported a range of changes in customer behaviours, including changes to buying behaviour, concerns about rising prices, a falloff in export sales, reactions to supply issues and changing expectations around lead times. For example:

“Customers have had to learn to adapt to supply issues.”

“Reduction in demand from some export customers.”

“Yes, some (customers are) looking at pulling the pin on new work due to prices continually increasing, some are having to settle for inferior, or not first choice materials due to availability issues.”

“People are more short-fused as products are harder to source from overseas. Everyone is learning to operate in the new normal with delays, longer timeframes and raising costs.”

Kiwi customers are more likely to be spending money on repairs, home renovations and domestic travel in response to a lack of offshore travel and spending opportunities. They are also becoming more price-conscious and clearer in their expectations when purchasing. For example:

“Customers are more demanding and less forgiving. Diplomacy and tact, as well as active listening skills, are needed.”

“Kiwis seem more cost-conscious in their spends.”

“More demanding and wanting quicker turnaround. More customers are asking for quotes before placing orders, even for just a small job.”

3.3 CASH FLOW AND WORKING CAPITAL

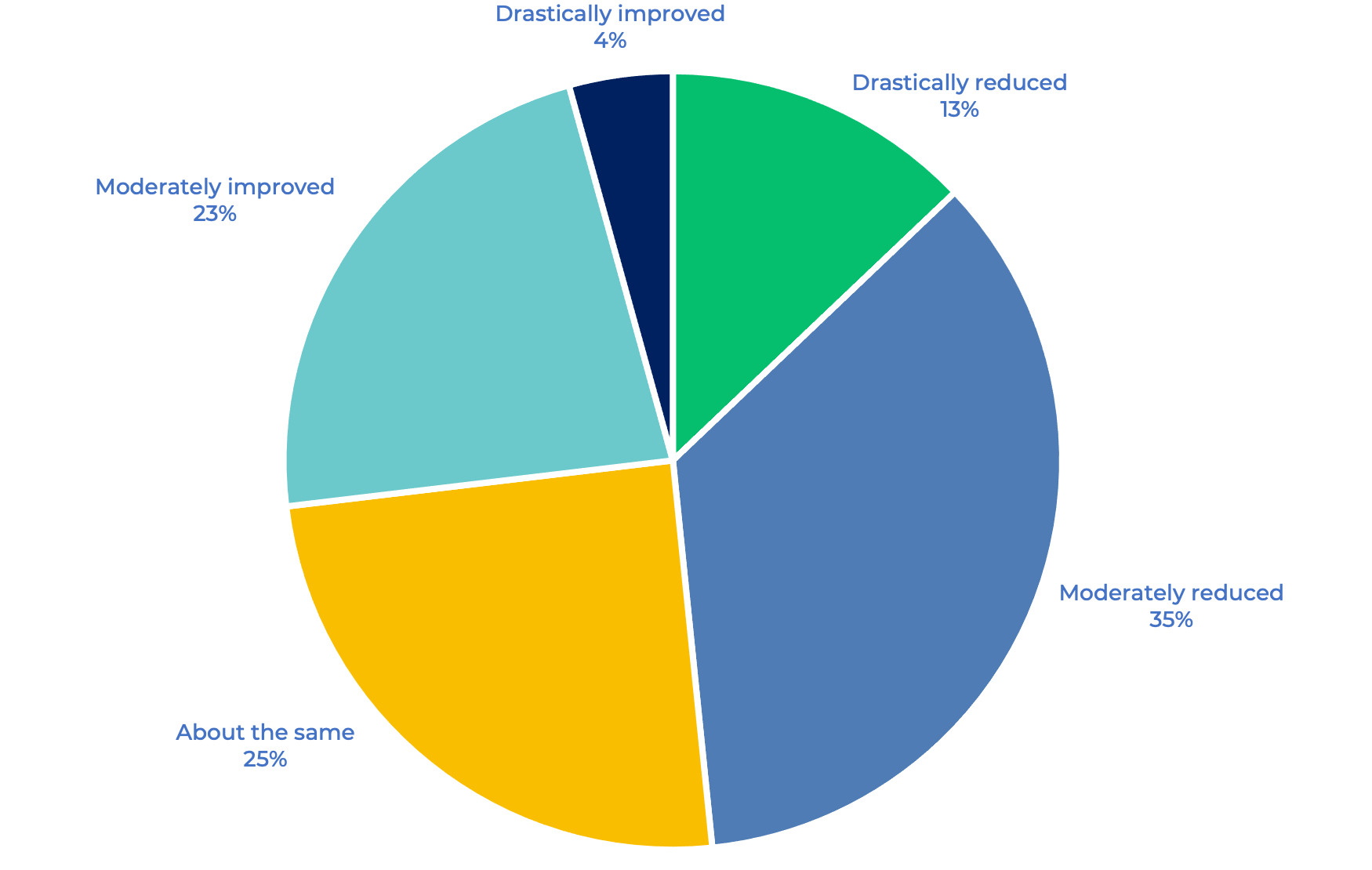

Just under half (48.9%) per cent of SMEs expect their cash flow to reduce either drastically (13%) or moderately (35.9%) during the next twelve-month period. Twenty-five per cent expects their cash flow to be about the same, while 22.8% expect a moderate improvement and 4.4% per cent expect a drastic improvement. This highlights some significant improvements from last year’s results where seventy per cent of respondents expected a decrease in cash flow, thirteen per cent expected no change, nine per cent expected a moderate improvement and eight per cent didn’t know.

How would you describe the likely impacts of the pandemic on your cash flow over the next 12 months?

67.4% of respondents think they will have an adequate amount of working capital to invest in plant, equipment and other assets during the next twelve months. 32.6% think they will not have enough working capital. Again, this represents an improvement from last year, where 43.5% thought they would have enough working capital, 28.3% thought they would not and 29.4% didn’t know.

In the next 12 months, will you have adequate working capital to invest in your business for plant, equipment and other vital assets?

3.4 INVESTMENT OPPORTUNITIES

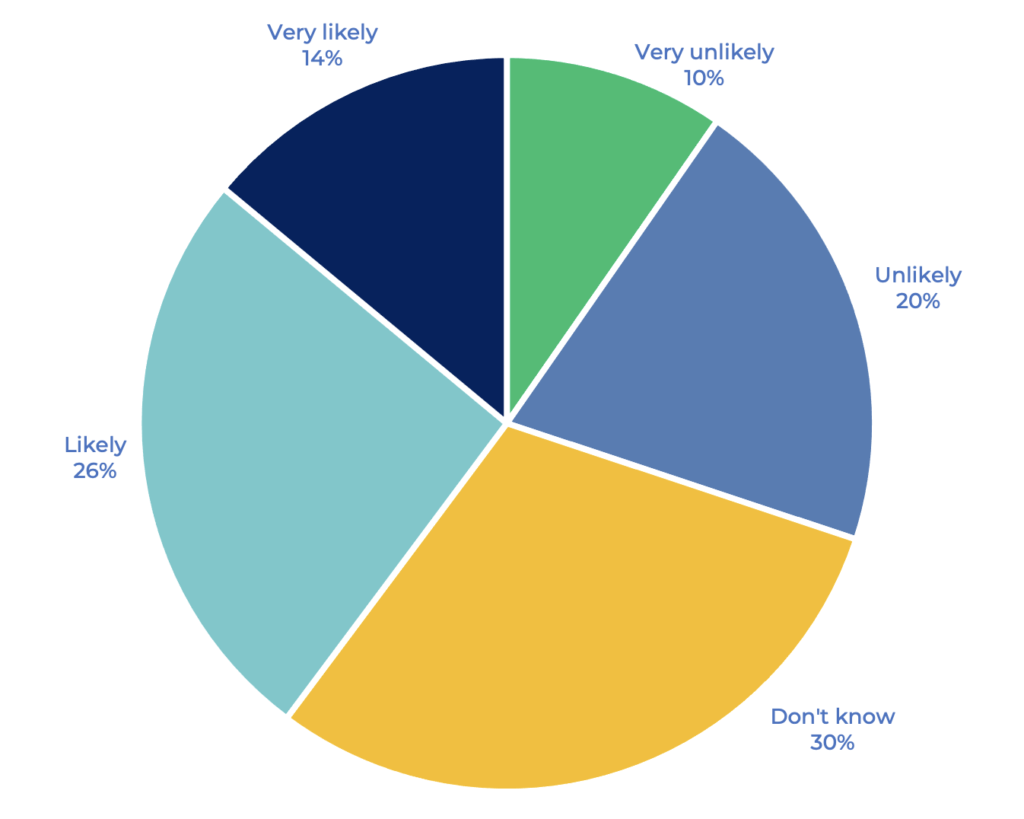

When considering how likely NZ small business owners are to invest in new opportunities, due to COVID, there was a mixed response. 30.4% didn’t know, 26.1% thought it likely, 20.7% thought it unlikely, 14.1% thought investment opportunities were very likely, 9.8% thought it very unlikely. There remains much uncertainty about investment opportunities in NZ as a result of COVID. There are significant differences, depending upon the industry sector businesses focus on.

How likely are you now to invest in new opportunities as a result of the pandemic?

3.5 UNEXPECTED OUTCOMES

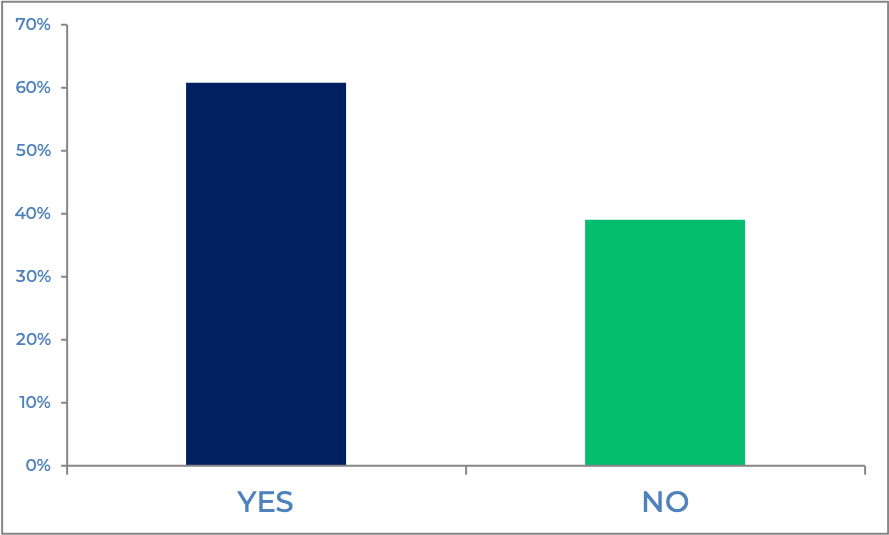

When asked about any unexpected positive outcomes for their business due to COVID, 60.9% replied that they had unexpected positive outcomes. 39.1% said they hadn’t. Again, this represents an improvement and more certainty compared with last year’s results, where 40.2% had unexpected positive outcomes and 54.4% did not.

Have there been any unexpected positive outcomes for your business as a result of the pandemic

Some businesses that did experience positive change reported doing more business due to their industry sector or location. For example:

“Higher profit margins due to downsizing staffing numbers and a constant workload throughout the year rather than seasonal.”

“New clients who have had to look for local suppliers due to problems with supply out of our area or overseas.”

“Better financial results than expected, and staff loyalty.”

Others were taking a more proactive approach to plan and change their businesses:

“Educational tourism as a greater focus on authenticity of experience which means better pre-trip information, slower and more deliberate on the ground management of groups and being more careful on how we present our country, culture and environment.”

“Domestic spend has increased with luxury items, like spa pools. No one is travelling internationally, so they are spending locally on their homes.”

“Better work-life balance with less travel required and more forced connectivity through regular Zoom/Teams with client suppliers and customers.”

3.6 USE OF TECHNOLOGY

For the majority (59.8%), the use of technology in their business has not changed because of COVID. However, 40.2% of respondents reported that changes in the use of technology have altered because of the crisis. These include more remote working from home, more use of online meeting programmes such as Zoom and Teams, more use of tablets for real-time field reporting, more online purchases and an increase in social media advertising of products.

Has the pandemic affected the use of technology in your business?

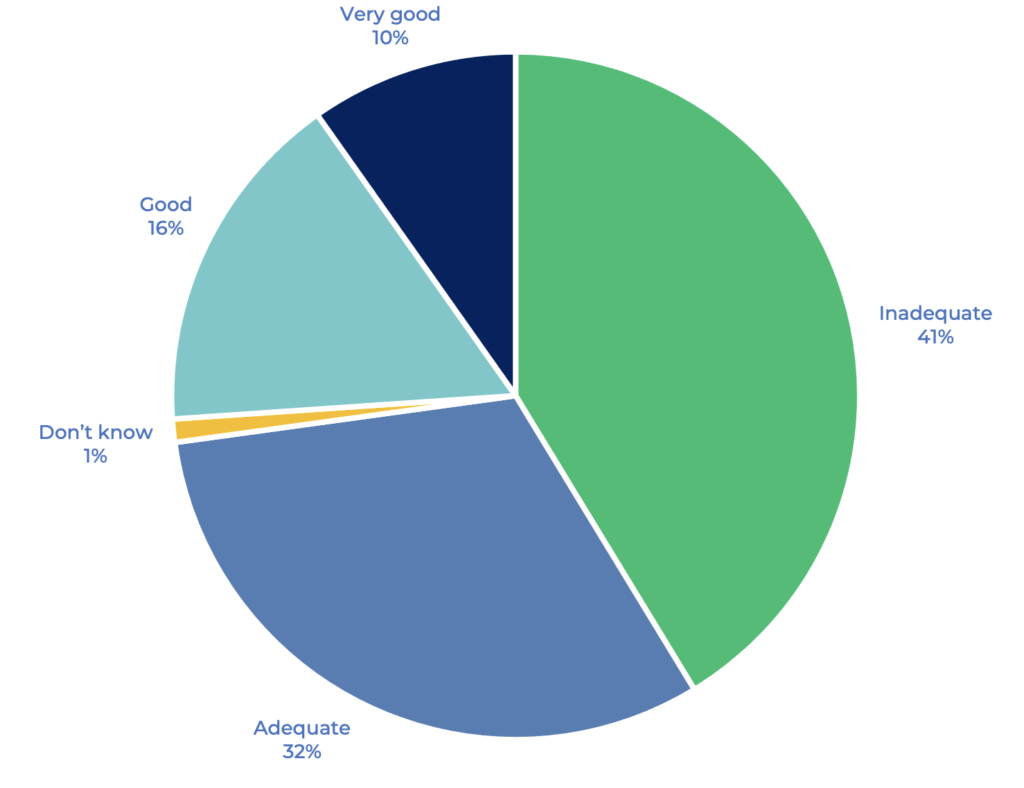

3.7 GOVERNMENT SUPPORT

Respondents were split when asked to describe levels of government support for small businesses during the COVID crisis. 41.3% described the support as inadequate, 31.5% thought the government response was adequate, 16.3% thought it was ‘good’, and 9.8% as ‘very good’.

The results represent a significantly reduced perception of government support for small businesses when compared with last year. At that time, 43.5% thought it was either ‘good’ or ‘very good’, 30% thought it was ‘adequate’, and 22% thought it was ‘inadequate’.

How would you describe levels of government support for small businesses coping with the pandemic during the past year?

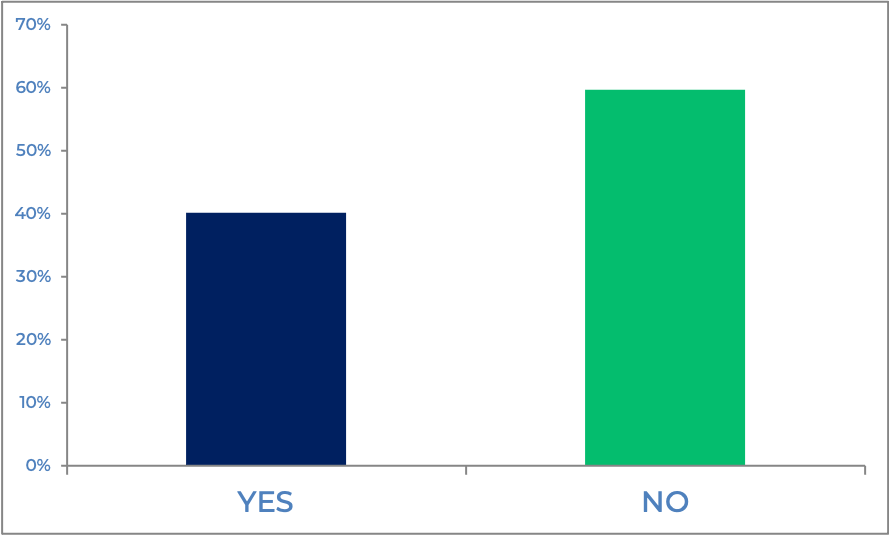

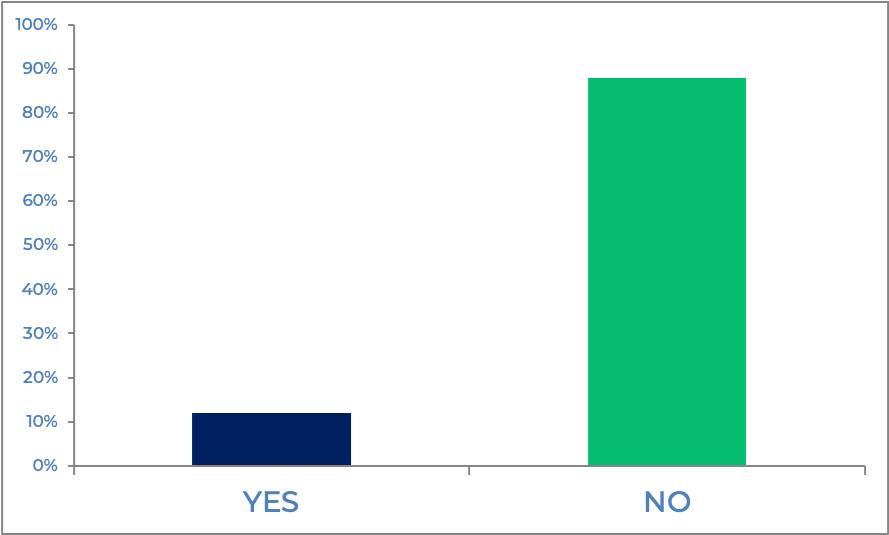

The role of central government intervention across the entire economy is a key factor in both mitigating and recovering from this global pandemic. Respondents were asked, “Do you think small and medium-sized businesses are represented adequately at the central government level?” Only twelve per cent replied yes, while eighty-eight per cent said no.

Again, this is significantly less than last year. Negative overall perceptions already showed, when 19.6% replied ‘yes’, 18.5% ‘didn’t yet know’, and 62% said ‘no’. Quite clearly, SMEs in New Zealand do not believe that central government has done enough to support them. Or represent their interests during the COVID crisis.

Do you think small and medium-sized businesses are represented adequately at the central government level?

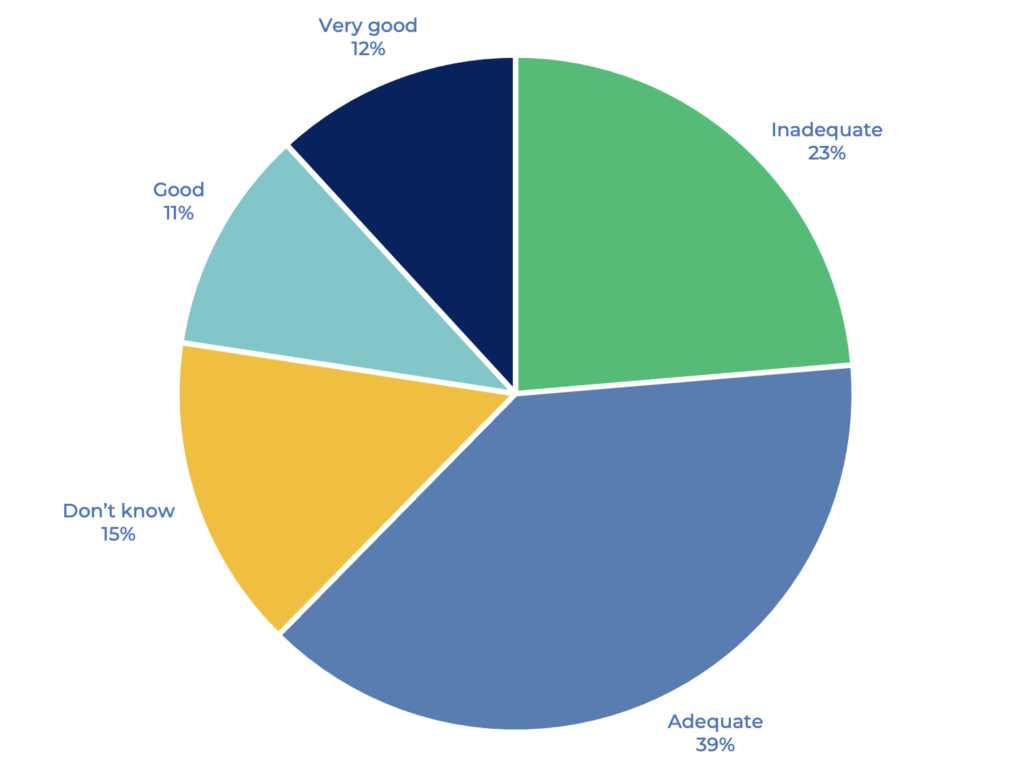

3.8 BANKING SECTOR SUPPORT

When asked to describe the level of support from the banking sector during the COVID crisis, there was a range of responses. 39.1% of respondents thought the response was ‘adequate’, 23.9% thought it was ‘inadequate’, 15.2 % ‘didn’t know’, 10.9% thought it was ‘good’, and 12% thought it was ‘very good’.

How would you describe the level of support from the banking sector during the pandemic over the past year?

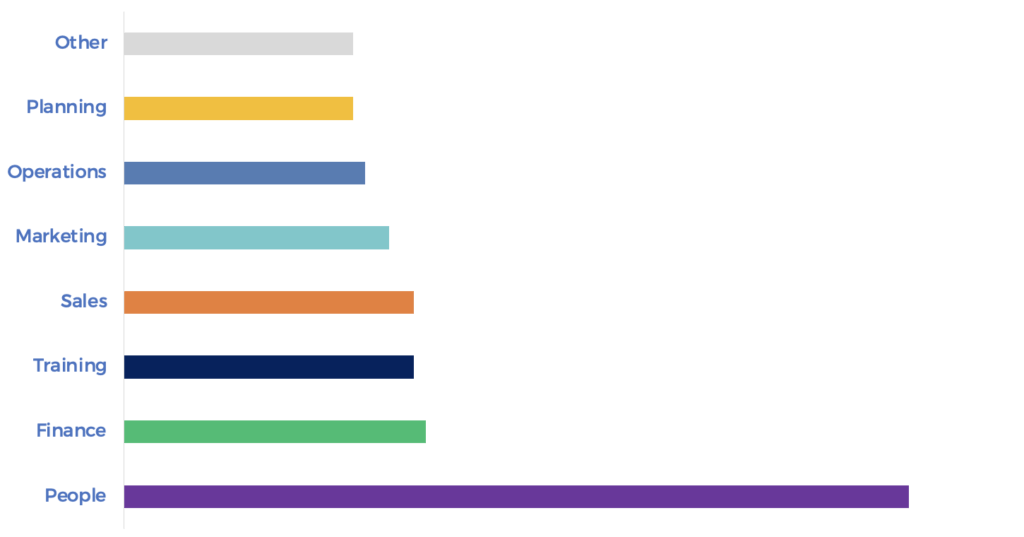

3.9 BUSINESS SUPPORT NEEDS

The previous survey was relatively soon after nationwide Level Two lockdown restrictions ended in 2020, and respondents were asked where they need the most support. This survey took place at the time of a suspended travel bubble with Australia, the early stages of vaccine roll out in NZ, and the rise of the Delta variant; which threatens the population with snap lockdowns if it takes hold.

In this context, small businesses identified their main needs in support as the following. People (70.6%), finance (27.2%), training (26.1%), sales (26.1%), marketing (23.9%), operations (21.7%) and planning (20.6%).

It marks a shift to more focus on people when compared to last year’s results. These included: Sales (38%) and marketing (35.9%) were the highest-rated followed by people (31.5%) and planning (31.5%), and finance (29.4%).

Thinking about your business coming through the pandemic, for which areas are you most needing support?

Conclusion

In mid-2020, the most concerns from small businesses related to a slow down of construction and infrastructure projects. This year, the key concern was around difficulties in global and domestic supply chains and major uncertainties around labour supply. Border closures have eliminated most international travel and, while there has been increased domestic Kiwi travel and local spending, there is an awareness that a significant slowdown in some sectors of the economy is ongoing. The flow-on effects of that slow down, while still being played out, continue to be very damaging for small businesses.

In 2021, small business owners reported that they had noticed some changes in consumer behaviour over the previous twelve months. These included changes to buying behaviour, concerns about rising prices, a falloff in export sales, reactions to supply issues and changing expectations around lead times. </sp

Just under half of SMEs expect their cash flow to reduce during the next twelve-month period. A quarter expects their cash flow to be about the same, while 27.2% expect an improvement. An upturn from last year’s results, where seventy per cent expected a decrease in cash flow, thirteen per cent expected no change, nine per cent expected a moderate improvement, and eight per cent didn’t know.

Approximately two-thirds of respondents think they will have adequate amounts to invest in plant, equipment and other assets during the next twelve months, while a third believe they will not have enough working capital. Again, this is an improvement from last year, where 43.5% thought they would have enough working capital, 28.3% thought they would not, and 29.4% didn’t know.

In terms of investing, approximately 60% of small businesses either did not know or were unlikely to invest. Whilst the other 40% were either likely or very likely to invest.

Overall, there remains much uncertainty about investment opportunities in NZ, as a result of COVID. There are significant differences; depending upon which industry sector businesses are involved.

Just over forty per cent of respondents reported that changes in technology use have altered because of the COVID crisis. These include more remote working from home, more use of online meeting programmes such as Zoom and Teams, more use of tablets for real-time field reporting, more online purchases, and increased social media advertising of products.

During 2021, small businesses have become less optimistic about government support for their sector. 41.3% described COVID support as ‘inadequate’, 31.5% thought the government response was ‘adequate’, 16.3% thought it was ‘good’, and 9.8% ‘very good’. Small businesses do not feel well represented at central government level, with eighty-eight per cent stating this position. At least from the perspective of small businesses, there is more work to be done by the government to support and represent this crucial sector of the NZ economy.

We hope you have found our Business Sentiment Survey useful. For more information contact:

Dr Dominic Moran | Partner | Business Advisor